UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File No. 001-16111

GLOBAL PAYMENTS INC.

(Exact name of registrant as specified in charter) |

| | |

Georgia | | 58-2567903 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

|

| | |

3550 Lenox Road, Atlanta, Georgia | | 30326 |

(Address of principal executive offices) | | (Zip Code) |

Registrant's telephone number, including area code: 770-829-8000

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

Title of each class | | Name of each exchange on which registered |

Common Stock, No Par Value | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

NONE

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer o

Non-accelerated filer o Smaller reporting company o

Emerging growth company o

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant's most recently completed second fiscal quarter was $13,694,503,028. The number of shares of the registrant's common stock outstanding at February 19, 2018 was 159,205,866 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Specifically identified portions of the registrant's proxy statement for the 2018 annual meeting of shareholders are incorporated by reference in Part III.

GLOBAL PAYMENTS INC.

2017 ANNUAL REPORT ON FORM 10-K

|

| | | |

| | | Page |

PART I |

ITEM 1. | | | |

ITEM 1A. | | | |

ITEM 2. | | | |

ITEM 3. | | | |

PART II |

ITEM 5. | | | |

ITEM 6. | | | |

ITEM 7. | | | |

ITEM 7A. | | | |

ITEM 8. | | | |

ITEM 9. | | | |

ITEM 9A. | | | |

PART III |

ITEM 10. | | | |

ITEM 11. | | | |

ITEM 12. | | | |

ITEM 13. | | | |

ITEM 14. | | | |

PART IV |

ITEM 15. | | | |

| | | |

EXPLANATORY NOTE REGARDING TRANSITION PERIOD

In 2016, we changed our fiscal year-end from May 31 to December 31. As a result, we refer to the period consisting of the seven-months ended December 31, 2016 as the "2016 fiscal transition period."

When our financial results for the year ended December 31, 2017 and the 2016 fiscal transition period are compared to our financial results for the prior-year periods, the results compare the twelve-month period from January 1, 2017 through December 31, 2017 to the twelve-month period from January 1, 2016 through December 31, 2016 and compare the seven-month period from June 1, 2016 through December 31, 2016 to the seven-month period from June 1, 2015 through December 31, 2015. The results for the twelve months ended December 31, 2016 and the seven months ended December 31, 2015 are unaudited.

CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

Unless the context requires otherwise, references in this report to "Global Payments," the "Company," "we," "our" or "us," refer to Global Payments Inc. and its subsidiaries.

We believe that it is important to communicate our plans for and expectations about the future to our shareholders and to the public. Some of the statements we use in this report, and in some of the documents we incorporate by reference in this report, contain forward-looking statements concerning our business operations, economic performance and financial condition, including in particular: our business strategy and means to implement the strategy; measures of future results of operations, such as revenues, expenses, operating margins, income tax rates, and earnings per share; other operating metrics such as shares outstanding and capital expenditures; our success and timing in developing and introducing new services and expanding our business; statements about the benefits of our acquisition of the communities and sports divisions of Athlaction Topco, LLC ("ACTIVE Network"), including future financial and operating results, the combined company’s plans, objectives, expectations and intentions, and the successful integration of future acquisitions. You can sometimes identify forward-looking statements by our use of the words "believes," "anticipates," "expects," "intends," "plan," "forecast," "guidance" and similar expressions. For these statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

Although we believe that the plans and expectations reflected in or suggested by our forward-looking statements are reasonable, those statements are based on a number of assumptions, estimates, projections or plans that are inherently subject to significant risks, uncertainties and contingencies, many of which are beyond our control, cannot be foreseen and reflect future business decisions that are subject to change. Accordingly, we cannot guarantee you that our plans and expectations will be achieved. Our actual revenues, revenue growth rates and margins, other results of operations and shareholder values could differ materially from those anticipated in our forward-looking statements as a result of many known and unknown factors, many of which are beyond our ability to predict or control. Important factors that may cause actual events or results to differ materially from those anticipated by our forward-looking statements include our ability to safeguard our data; increased competition from larger companies and non-traditional competitors; our ability to update our services in a timely manner; our ability to maintain Visa and MasterCard registration and financial institution sponsorship; our reliance on financial institutions to provide clearing services in connection with our settlement activities; our potential failure to comply with card network requirements; potential systems interruptions or failures; software defects or undetected errors; increased attrition of merchants, referral partners or independent sales organizations; our ability to increase our share of existing markets and expand into new markets; a decline in the use of cards for payment generally; unanticipated increases in chargeback liability; increases in credit card network fees; changes in laws, regulations or network rules or interpretations thereof; foreign currency exchange and interest rate risks; political, economic and regulatory changes in the foreign countries in which we operate; future performance, integration and conversion of acquired operations, including without limitation difficulties and delays in integrating or fully realizing cost savings and other benefits of our acquisitions at all or within the expected time period; fully realizing anticipated annual interest expense savings from refinancing our Credit Facility; loss of key personnel; and other risk factors presented in Item "1A - Risk Factors of this Annual Report on Form 10‑K," which we advise you to review. These cautionary statements qualify all of our forward-looking statements, and you are cautioned not to place undue reliance on these forward-looking statements.

Our forward-looking statements speak only as of the date they are made and should not be relied upon as representing our plans and expectations as of any subsequent date. While we may elect to update or revise forward-looking statements at some time in the future, we specifically disclaim any obligation to publicly release the results of any revisions to our forward-looking statements.

PART I

ITEM 1- BUSINESS

Introduction

We are a leading worldwide provider of payment technology and software solutions delivering innovative services to our customers globally. Our technologies, services and employee expertise enable us to provide a broad range of solutions that allow our customers to accept various payment types and operate their businesses more efficiently. We distribute our services across a variety of channels to customers in 30 countries throughout North America, Europe, the Asia-Pacific region and Brazil and operate in three reportable segments: North America, Europe and Asia-Pacific.

We were incorporated in Georgia as Global Payments Inc. in 2000 and spun-off from our former parent company in 2001. Including our time as part of our former parent company, we have been in the payment technology services business since 1967. Since our spin-off, we have grown our annual revenues from $353 million for the year ended May 31, 2001 to $4.0 billion for the year ended December 31, 2017, through internal expansion of existing operations and through acquisitions.

Headquartered in Atlanta, Georgia, we are a member of the Standard & Poor's 500 Index, and our common stock is traded on the New York Stock Exchange under the symbol "GPN."

Recent Developments

On September 1, 2017, we acquired ACTIVE Network for total purchase consideration of $1.2 billion, consisting of approximately $600 million in cash and 6.4 million shares of our common stock. ACTIVE Network delivers cloud-based enterprise software, including payment technology solutions, to event organizers in the communities and health and fitness vertical markets. This acquisition aligns with our technology-enabled, software driven strategy and adds an enterprise software business operating in two additional vertical markets that we believe offer attractive growth fundamentals. On April 22, 2016, we merged with Heartland Payment Systems, Inc. ("Heartland") in a cash-and-stock transaction for total purchase consideration of $3.9 billion. The merger significantly expanded our small and medium-sized enterprise distribution, merchant base and vertical reach in the United States. See "Note 2—Acquisitions" in the notes to the accompanying consolidated financial statements for further discussion of these and other acquisitions.

On May 2, 2017, we amended our existing corporate credit facility (the "Credit Facility") to increase the total financing capacity available under the Credit Facility to $5.2 billion. As of December 31, 2017, the Credit Facility provided for secured financing compromised of (i) a $1.5 billion term loan (the "Term A Loan"), (ii) a $1.3 billion term loan (the "Term A-2 Loan"), (iii) a $1.2 billion term loan facility (the "Term B-2 Loan") and (iv) a $1.25 billion revolving credit facility (the "Revolving Credit Facility"). See "Management's Discussion and Analysis - Liquidity and Capital Resources - Long-Term Debt and Lines of Credit" below for further discussion of our credit facilities.

Payment Technology Services and Software Solutions Overview

We provide payment technology and software solutions to customers globally. Our payment solutions are similar around the world in that we enable our customers to accept card, electronic, check and digital-based payments. Our comprehensive offerings include, but are not limited to, authorization services, settlement and funding services, customer support and help-desk functions, chargeback resolution, terminal rental, sales and deployment, payment security services, consolidated billing and statements and on-line reporting.

In addition, we offer a wide array of enterprise software solutions that streamline business operations to customers in numerous vertical markets. We also provide a variety of value-added services, including analytic and engagement tools, payroll services and reporting that assist our customers with driving demand and operating their businesses more efficiently.

Our value proposition is to provide distinctive high-quality, responsive and secure services to all of our customers. We distribute our services through multiple channels and target customers in many vertical markets in 30 countries located throughout North America, Europe, the Asia-Pacific region and in Brazil. The majority of revenues is generated by services priced as a percentage of transaction value or a specified fee per transaction, depending on the card type or the market. We also earn software licensing and subscription fees and other fees based on specific value-added services that may be unrelated to the number or value of transactions.

Direct Distribution

Our primary business model is to actively market and provide our payment services, enterprise software solutions and other value-added services directly to our customers through a variety of distribution channels. We offer high touch services that provide our customers with reliable and secure solutions coupled with high quality and responsive support services. Through our direct sales force worldwide, as well as bank partnerships, we offer our payment technology services, software and other value-added solutions directly to customers in the markets we serve. See "Business Segments" below for a description of our direct sales forces located around the world.

Many of our payment solutions are technology-enabled in that they incorporate or are incorporated into innovative, technology-driven solutions, including enterprise software solutions, designed to enable merchants to better manage their businesses. Our primary technology-enabled solutions include integrated and vertical markets, ecommerce and omnichannel and gaming solutions, each as described below.

Integrated and Vertical Markets. Our integrated and vertical market solutions provide advanced payments technology that is deeply integrated into business enterprise software solutions either owned by us or by our partners. We grow our business when new merchants implement our enterprise software solutions and when new or existing merchants enable payments services through enterprise software solutions sold by us or by our partners. We distribute our integrated payment solutions primarily through the following businesses:

| |

• | OpenEdge. Through OpenEdge, we offer integrated payment solutions through more than 2,000 technology partners across over 60 different verticals primarily in North America. OpenEdge enables third-party application developers to incorporate payment innovations into their enterprise business solutions. |

| |

• | Ezidebit. Through Ezi Holdings Pty Ltd ("Ezidebit"), we offer integrated payment solutions in the Asia-Pacific region. Ezidebit focuses on recurring payments verticals and, similar to OpenEdge, markets its services through a network of integrated software vendors and direct channels to numerous vertical markets. |

| |

• | ACTIVE Network. Through ACTIVE Network, we deliver cloud-based enterprise software, including payment technology solutions, to event organizers in the communities and health and fitness markets. |

| |

• | Education Solutions. We offer integrated payment solutions specifically designed for all levels of educational institutions. At the university level, we offer integrated commerce solutions, payment services, higher education loan services and open- and closed-loop payment solutions. For kindergarten through 12th grade, we provide ecommerce and in-person payments, cafeteria POS solutions and back-office management software, hardware, technical support and training. |

| |

• | Point-of-Sale Solutions. We offer leading-edge POS software solutions, integrated with our payment services and other adjacent business service applications, which may be on-premise or cloud-based, targeted primarily at the hospitality and retail verticals. |

Ecommerce and Omnichannel. We offer ecommerce and omnichannel solutions to our customers that seamlessly blend payment gateway services, retail payment acceptance infrastructure and payment technology service capabilities to allow merchants to accept various payment methods through any channel across our geographical footprint. We sell ecommerce and omnichannel solutions to customers of all sizes, from small businesses accepting payments in a single country, to enterprise and multinational businesses that have complex payment needs and operate retail and online businesses in multiple countries.

Gaming. We offer a comprehensive suite of cash access solutions to the gaming market in North America. These solutions include credit and debit card cash advance, traditional and electronic check processing and other services specific to this market. Our services allow casino patrons in North America fast access to cash with high limits to enable gaming establishments to increase the flow of money to their gaming floors and reduce risk.

Wholesale Distribution

Although our primary business model is to build high quality direct relationships with merchants, we also provide our services through a wholesale distribution channel where we do not maintain the face-to-face relationship with the merchant. Through our wholesale channel, we provide payment services to merchants through independent sales organizations ("ISOs"). The ISOs act as third-party sales groups selling our payment technology services directly to end-user merchant customers.

Credit and Debit Card Transaction Processing

Credit and debit card transaction processing includes the processing of the world's major international card brands, including American Express, Discover Card ("Discover"), JCB, MasterCard, UnionPay International ("UPI"), Visa and non-traditional payment methods, as well as certain domestic debit networks, such as Interac in Canada. Credit and debit networks establish uniform regulations that govern much of the payment card industry. During a typical payment transaction, the merchant and the card issuer do not interface directly with each other, but instead rely on payments technology companies, such as Global Payments, to facilitate transaction processing services, including authorization, electronic draft capture, file transfers to facilitate funds settlement and certain exception-based, back office support services such as chargeback and retrieval resolution.

We process funds settlement under two models, a sponsorship model and a direct membership model. Under the sponsorship model, we are designated as a Merchant Service Provider by MasterCard and as an ISO by Visa. To be designated as a certified processor, member clearing financial institutions ("Member") sponsor us and require our adherence to the standards of the networks. In certain markets, we have sponsorship or depository and clearing agreements with financial institution sponsors. These agreements allow us to route transactions under the Members' control and identification numbers to clear card transactions through MasterCard and Visa. In this model, the standards of the card networks restrict us from performing funds settlement or accessing merchant settlement funds, and, instead, require that these funds be in the possession of the Member until the merchant has been funded.

Under the direct membership model, we are direct members in various payment networks, allowing us to process and fund transactions without third-party sponsorship. In this model, we route and clear transactions directly through the card brand’s network and are not restricted from performing funds settlement. Otherwise, we process these transactions similarly to how we process transactions in the sponsorship model. We are required to adhere to the standards of the various networks in which we are direct members. We maintain relationships with financial institutions, which may also serve as our Member sponsors for other card brands or in other markets, to assist with funds settlement.

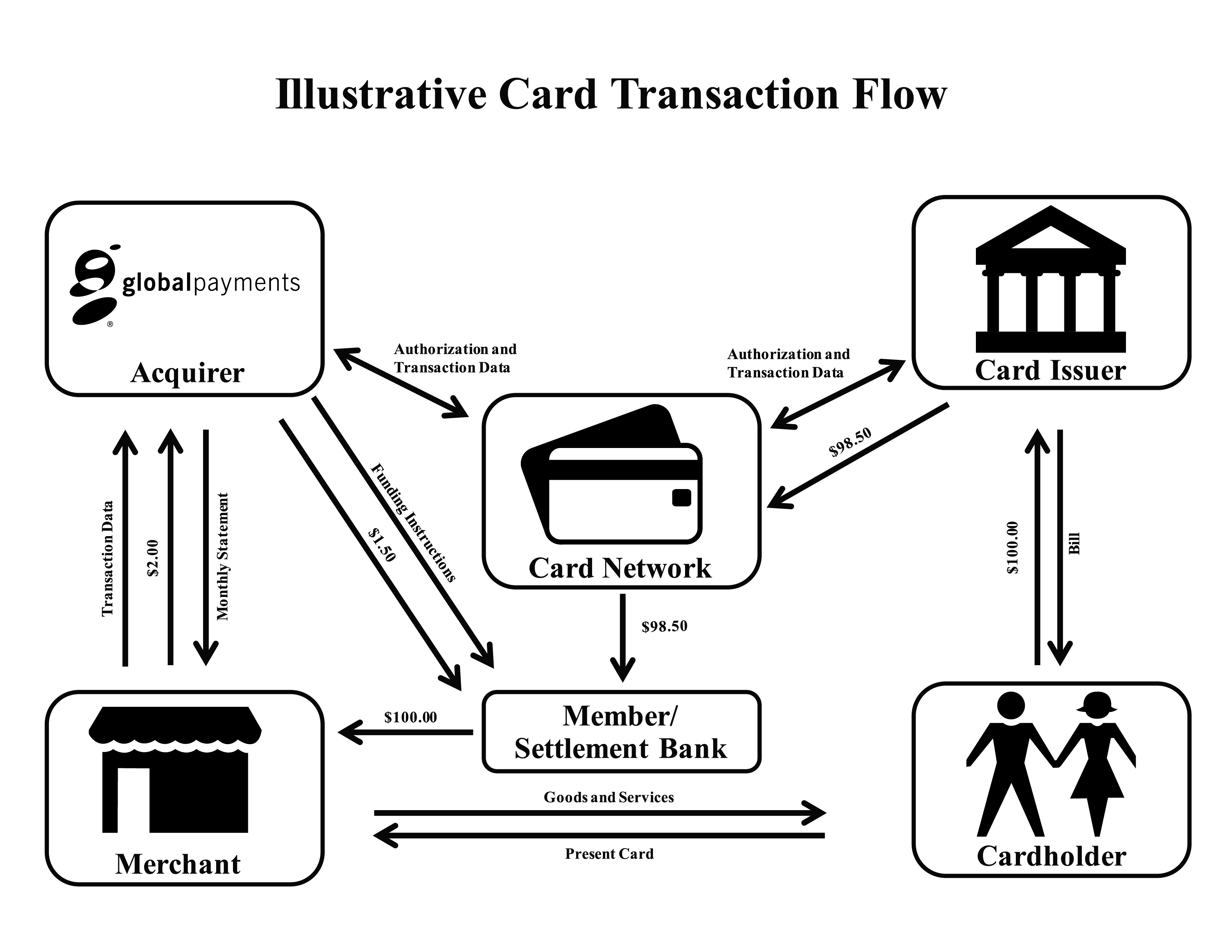

How a Card Transaction Works

A typical payment transaction begins when a cardholder presents a card for payment at a merchant location where the card information is captured by a POS terminal card reader or mobile device card reader, which may be sold or leased to the merchant and serviced by us. Alternatively, card and transaction information may be captured and transmitted to our network through a POS device or ecommerce portal by one of a number of services that we offer directly or through a value-added reseller. The card reader electronically records sales draft information, such as the card identification number, transaction date and transaction amount.

After the card and transaction information is captured, the POS device automatically connects to our network through the internet or other communication channel in order to receive authorization of the transaction. For a credit card transaction, authorization services generally refer to the process in which the card issuer indicates whether a particular credit card is authentic and whether the impending transaction amount will cause the cardholder to exceed defined credit limits. In a debit card transaction, we obtain authorization for the transaction from the card issuer through the payment network verifying that the cardholder has sufficient funds for the transaction amount.

As an illustration, shown below, on a $100.00 card transaction, the card issuer may fund the Member, our sponsor, (indirectly through the card network) $98.50 after retaining approximately $1.50 referred to as an interchange fee. The card issuer seeks reimbursement of $100.00 from the cardholder in the cardholder's monthly credit card statement. The Member would, in turn, pay the merchant $100.00. The net settlement after this transaction would require us to advance the Member $1.50. After the end of the month, we would bill the merchant a percentage of the transaction amount, or merchant discount, to cover the full amount of the interchange fee and our fee from the transaction. If our discount rate for the merchant in the above example was 2.00%, we would bill the merchant $2.00 after the end of the month for the transaction, reimburse ourselves for $1.50 in interchange fees and retain $0.50 as our fees for the transaction. Under some arrangements, we remit the net amount of $98.50 to the merchant, rather than funding the full $100.00 and subsequently billing the merchant at the end of the month. Discount rates vary based on negotiations with merchants and the economic characteristics of transactions. Interchange rates also vary based on the economic characteristics of individual transactions. Accordingly, our fee per transaction varies across our merchant base and is subject to change based on changes in discount rates and interchange rates. Our profit on the transaction reflects the fee received less operating expenses, including payment network fees, systems cost to process the transaction and commissions paid to our sales force or ISO. Payment network fees are charged by the card brands based on the value of transactions processed through their networks.

Business Segments

We operate in three reportable segments: North America, Europe and Asia-Pacific. See "Note 15—Segment Information" in the notes to the accompanying consolidated financial statements for additional information about our segments, including revenues, operating income and depreciation and amortization by segment as well as financial information about geographic areas in which we operate. Our foreign operations subject us to various risks, including, without limitation, currency exchange risks and political, economic and regulatory risks. See "Item 1A - Risk Factors" for additional information about these risks.

North America

Approximately 73.7% of our revenues for the year ended December 31, 2017 were derived from our operations in North America, which include the United States and Canada.

Our primary mode of distribution in North America is our direct distribution channels, including an extensive direct sales force selling our services and solutions across numerous vertical markets, including, but not limited too, education, restaurant, event management, hospitality, retail, healthcare, convenience stores and petroleum, professional services, automotive and lodging.

In addition, our technology-enabled solutions represented a substantial component of our revenues in North America for the year ended December 31, 2017. Our technology-enabled distribution in North America primarily includes integrated and vertical market solutions as well as our gaming solutions business.

We also generate a portion of our revenues in North America from our wholesale distribution channel, primarily ISOs acting as third-party selling groups.

Europe

Approximately 19.3% of our revenues for the year ended December 31, 2017 were derived from our operations in Europe, which includes the United Kingdom, the Republic of Ireland, Spain, the Republic of Malta, the Czech Republic, Hungary, Slovakia, Romania and the Russian Federation. We have direct sales forces in these markets through which we sell our services

while also leveraging our bank referral relationships. Our ecommerce and omnichannel solutions represent a growing percentage of the services we sell in Europe.

Asia-Pacific

Approximately 7.0% of our revenues for the year ended December 31, 2017 were derived from our operations in the Asia-Pacific region, which includes the following countries and territories: Australia, China, Hong Kong, India, Macau, Malaysia, Maldives, New Zealand, the Philippines, Singapore, Sri Lanka and Taiwan. Our direct sales force in the Asia-Pacific region accounts for substantially all of the services we sell in the region.

Technology-enabled solutions represent a substantial and growing portion of our operations in the Asia-Pacific region, driven by Ezidebit in Australia. Our acquisition of eWay Limited in April 2016 has allowed us to further expand our ecommerce and omnichannel solutions offerings in this region.

Industry Overview

The payment technology services industry provides merchants with credit, debit, gift and loyalty card and other payment processing services, along with related information services. The industry continues to grow as a result of wider merchant acceptance, increased consumer use of credit and debit cards and advances in payment processing and telecommunications technology. The proliferation of credit and debit cards has made the acceptance of card-based payments a virtual necessity for many businesses, regardless of size, in order to remain competitive. This increased use of cards and the availability of more sophisticated technology services to all market segments has resulted in a highly competitive and specialized industry.

Competition

We are a leading provider of payments technology services in North America, where we compete primarily with Bank of America Merchant Services, LLC (a joint venture between First Data Corporation and Bank of America Corporation), Chase Paymentech Solutions, LLC, Elavon, Inc., a subsidiary of U.S. Bancorp, First Data Corporation, Total System Services, Inc., Wells Fargo Bank, N.A and Worldpay, Inc. While these are our primary competitors, some of our vertically focused business in the United States compete with other organizations.

In Europe and the Asia-Pacific region, financial institutions remain the primary providers of payment services to merchants, although the outsourcing of these services to third-party service providers is becoming more prevalent. Payment services have become increasingly complex, requiring significant capital commitments to develop, maintain and update the systems necessary to provide these advanced services at competitive prices.

Competitors in Europe include Barclays Bank PLC, Spanish banking institutions and WorldPay, Inc. Financial institutions that offer merchant acquiring services are our primary competitors in Asia-Pacific.

Emerging Trends

The payments industry continues to grow worldwide and as a result, certain large payment technology companies, including us, have expanded operations globally by pursuing acquisitions and creating alliances and joint ventures. We expect to continue to expand into new markets internationally or increase our scale and improve our competitiveness in existing markets by pursuing further acquisitions and joint ventures.

We believe that the number of electronic payment transactions will continue to grow and that an increasing percentage of these will be facilitated through emerging technologies. As a result, we expect an increasing portion of our future capital investment will be allocated to support the development of new and emerging technologies; however, we do not expect our aggregate capital spending to increase materially from our current level of spending as a result of this.

We also believe new markets will continue to develop in areas that have been previously dominated by paper-based transactions. We expect industries such as education, government and healthcare, as well as recurring payments and business-to-business payments, to continue to see transactions migrate to electronic-based solutions. We anticipate that the continued development of new services and the emergence of new vertical markets will be a factor in the growth of our business and our revenue in the future.

Strategy

We seek to leverage the adoption of, and transition to, card, electronic and digital-based payments by expanding share in our existing markets through our distribution channels and service innovation, as well as through acquisitions to improve our offerings and scale, while also seeking to enter new markets through acquisitions, alliances and joint ventures around the world. We intend to continue to invest in and leverage our technology infrastructure and our people to increase our penetration in existing markets.

Our key objectives include the following:

| |

• | Grow and control our direct distribution by adding new channels and partners, including expanding our ownership of additional enterprise software solutions in select vertical markets; |

| |

• | Deliver innovative services by developing value-added applications, enhancing existing services and developing new systems and services to blend technology with customer needs; |

| |

• | Leverage technology and operational advantages throughout our global footprint; |

| |

• | Continue to develop seamless multinational solutions for leading global customers; |

| |

• | Provide customer service at levels that exceed our competition, while investing in technology, training and enhancements to our service offerings; and |

| |

• | Pursue potential domestic and international acquisitions of, investments in and alliances with companies that have high growth potential, significant market presence, sustainable distribution platforms and/or key technological capabilities. |

Competitive Strengths

We believe that our competitive strengths include the following:

| |

• | Global Footprint and Distribution - Our worldwide presence allows us to focus our investments on markets with promising gross domestic product fundamentals and favorable secular trends, makes us more attractive to merchants with international operations and exposes us to emerging innovations that we can adopt globally, while diversifying our economic risk. |

| |

• | Technology Solutions - We provide innovative technology-based solutions, including enterprise software solutions, that enable our customers to operate their business more efficiently and simplify the payments process, regardless of the channel through which the transaction occurs. We believe our robust technology solutions will continue to differentiate us in the marketplace and will position us for continued growth. |

| |

• | Scalable Operating Environment and Technology Infrastructure - We operate as a single, unified international organization, with a multi-channel, global technology infrastructure, which provides scalable and innovative service offerings and a consistent service experience to our merchants and partners worldwide, while also driving sustainable operating efficiencies. |

| |

• | Strong, Long-lasting Partner Relationships - We have established strong, long-lasting relationships with many financial institutions, enterprise software providers, value-added resellers and other technology-based payment service providers, which facilitate lead generation and enable us to deliver a diverse solutions set to our merchant customers. |

| |

• | Disciplined Acquisition Approach - Our proven track record for selectively and successfully sourcing, completing and integrating acquired businesses in existing and new markets positions us well for future growth and as an attractive partner for potential acquisition targets. |

Safeguarding Our Business

Privacy and security are central to our services. We work with information security and forensics firms and employ advanced technologies to prevent, investigate and address issues relating to processing system security and availability. We also collaborate with industry third parties, regulators and law enforcement to resolve security incidents and assist in efforts to prevent unauthorized access to our processing systems.

Employees and Labor

As of December 31, 2017, we had approximately 10,000 employees, many of whom are highly skilled in technical areas specific to payment technology services.

Regulation

Various aspects of our business are subject to regulation and supervision under federal, state and local laws in the United States, as well as foreign laws, regulations and rules. In addition, we are subject to rules promulgated by the various payment networks, including American Express, Discover, Interac, MasterCard, UPI and Visa; Directive 2007/64/EC in the European Union (the "Payment Services Directive"); as well as a variety of other regulations, including escheat laws and applicable privacy and information security regulations. In addition, because we provide data processing services to banks and other financial institutions, we are subject to examination by the Federal Financial Institutions Examination Council (the "FFIEC"). Set forth below is a brief summary of some of the significant laws and regulations that apply to us. These descriptions are not exhaustive, and these laws, regulations and rules frequently change.

Dodd-Frank Act

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the "Dodd-Frank Act"), which was signed into law in the United States in 2010, resulted in significant structural and other changes to the regulation of the financial services industry. The Dodd-Frank Act directed the Board of Governors of the Federal Reserve (the "Federal Reserve Board") to regulate the debit interchange transaction fees that a card issuer or payment card network receives or charges for an electronic debit transaction. Pursuant to the so-called "Durbin Amendment" to the Dodd-Frank Act, these fees must be "reasonable and proportional" to the cost incurred by the card issuer in authorizing, clearing and settling the transaction. Pursuant to regulations promulgated by the Federal Reserve Board, debit interchange rates for card issuers with assets of $10 billion or more are capped at $0.21 per transaction and an ad valorem component of 5 basis points to reflect a portion of the issuer's fraud losses plus, for qualifying issuers, an additional $0.01 per transaction in debit interchange for fraud prevention costs. The cap on interchange fees has not had a material direct effect on our results of operations.

In addition, the Dodd-Frank Act limits the ability of payment card networks to impose certain restrictions because it allows merchants to: (i) set minimum dollar amounts (not to exceed $10) for the acceptance of a credit card (and allows federal governmental entities and institutions of higher education to set maximum amounts for the acceptance of credit cards) and (ii) provide discounts or incentives to encourage consumers to pay with cash, checks, debit cards or credit cards.

The rules also contain prohibitions on network exclusivity and merchant routing restrictions that require a card issuer to enable at least two unaffiliated networks on each debit card, prohibit card networks from entering into exclusivity arrangements and restrict the ability of issuers or networks to mandate transaction routing requirements. The prohibition on network exclusivity has not significantly affected our ability to pass on network fees and other costs to our customers, nor do we expect it to in the future.

The Dodd-Frank Act also created the Financial Stability Oversight Council (the "FSOC"), which was established to, among other things, identify risks to the stability of the U.S. financial system. The FSOC has the authority to require supervision and regulation of nonbank financial companies that the FSOC determines pose a systemic risk to the U.S. financial system. Accordingly, we may be subject to additional systemic risk-related oversight.

Payment Network Rules

We are subject to the rules of American Express, Discover, Interac, MasterCard, UPI and Visa and other payment networks. In order to provide our services, several of our subsidiaries are either registered as service providers for member institutions with MasterCard, Visa and other networks or are direct members of MasterCard, Visa and other networks. Accordingly, we are subject to card association and network rules that could subject us to a variety of fines or penalties that may be levied by the card networks for certain acts or omissions.

Banking Laws and Regulations

The FFIEC is an interagency body comprised of federal bank and credit union regulators such as the Federal Reserve Board, the Federal Deposit Insurance Corporation, the National Credit Union Administration, the Office of the Comptroller of the Currency and the Bureau of Consumer Financial Protection. The FFIEC examines large data processors in order to identify and mitigate risks associated with systemically significant service providers, including specifically the risks they may pose to the banking industry. In addition, we are subject to the Payment Services Directive, which was implemented in most European Union member states through national legislation. As a result of this legislation, we are subject to regulation and oversight in certain European Union member nations, including the requirement that we maintain specified regulatory capital; however, these regulatory capital requirements are generally insignificant to our total assets and total equity and have no material effect on our liquidity.

Privacy and Information Security Laws

We provide services that may be subject to various state, federal and foreign privacy laws and regulations. These laws and regulations include the federal Gramm-Leach-Bliley Act of 1999, which applies to a broad range of financial institutions and to companies that provide services to financial institutions in the United States, including our gaming business. We are also subject to a variety of foreign data protection and privacy laws, including, without limitation, Directive 95/46/EC, as implemented in each member state of the European Union and its successor, the General Data Protection Regulation, which becomes effective in May 2018. Among other things, these foreign and domestic laws, and their implementing regulations, in certain cases restrict the collection, processing, storage, use and disclosure of personal information, require notice to individuals of privacy practices, and provide individuals with certain rights to prevent use and disclosure of protected information. These laws also impose requirements for safeguarding and removal or elimination of personal information.

Anti-Money Laundering and Counter Terrorist Requirements

In many countries, we are legally or contractually required to comply with anti-money laundering laws and regulations, such as, in the United States, the Bank Secrecy Act, as amended by the USA PATRIOT Act of 2001 (collectively, the "BSA"), and the BSA implementing regulations of the Financial Crimes Enforcement Network ("FinCEN"), a bureau of the U.S. Department of the Treasury. A variety of similar anti-money laundering requirements apply in other countries. In some countries, we are directly subject to these requirements; in other countries, we have contractually agreed to assist our sponsor banks with their obligation to comply with anti-money laundering requirements that apply to them. These laws typically require organizations to:

| |

• | establish and audit anti-money laundering programs; |

| |

• | establish procedures for obtaining and verifying customer information; |

| |

• | file reports on large cash transactions; and |

| |

• | file suspicious activity reports if the financial institution believes a customer may be violating U.S. laws and regulations. |

Regulations issued by the Office of Foreign Assets Control ("OFAC") of the U.S. Department of Treasury place prohibitions and restrictions on all U.S. citizens and entities, including the Company, with respect to transactions by U.S. persons with specified countries and individuals and entities identified on OFAC's Specially Designated Nationals list (for example, individuals and companies owned or controlled by, or acting for or on behalf of, countries subject to certain economic and trade sanctions, as well as terrorists, terrorist organizations and narcotics traffickers identified by OFAC under programs that are not country specific). Similar requirements apply to transactions and dealings with persons and entities specified in lists maintained in other countries. We have developed procedures and controls that are designed to monitor and address legal and regulatory requirements and developments and that allow our customers to protect against having direct business dealings with such prohibited countries, individuals or entities.

Escheat Laws

We are subject to unclaimed or abandoned property state laws in the United States and in certain foreign countries that require us to transfer to certain government authorities the unclaimed property of others that we hold when that property has

been unclaimed for a certain period of time. Moreover, we are subject to audit by state and foreign regulatory authorities with regard to our escheatment practices.

Foreign Laws and Regulations

We are subject to foreign laws and regulations that affect the electronic payments industry in each of the foreign countries in which we operate. Some of these countries, such as the Russian Federation and the United Kingdom, have undergone significant political, economic and social change in recent years. In these countries, there is a greater risk of new, unforeseen changes that could result from, among other things, instability or changes in a country’s or region’s economic conditions; changes in laws or regulations or in the interpretation of existing laws or regulations, whether caused by a change in government or otherwise; increased difficulty of conducting business in a country or region due to actual or potential political or military conflict; or action by the European Union or the United States, Canada or other governments that may restrict our ability to transact business in a foreign country or with certain foreign individuals or entities, such as sanctions by or against the Russian Federation.

Debt Collection and Credit Reporting Laws

Portions of our business may be subject to the Fair Debt Collection Practices Act, the Fair Credit Reporting Act and similar state laws. These debt collection laws are designed to eliminate abusive, deceptive and unfair debt collection practices and may require licensing at the state level. The Fair Credit Reporting Act regulates the use and reporting of consumer credit information and also imposes disclosure requirements on entities that take adverse action based on information obtained from credit reporting agencies. We have procedures in place to comply with the requirements of these laws.

Where to Find More Information

We file annual and quarterly reports, proxy statements and other information with the U.S. Securities and Exchange Commission (the "SEC"). You may read and print materials that we have filed with the SEC from its website at www.sec.gov. In addition, certain of our SEC filings, including our annual reports on Form 10-K, our transition report on Form 10-K for the 2016 fiscal transition period, our quarterly reports on Form 10-Q, our current reports on Form 8-K and amendments to them can be viewed and printed from the investor relations section of our website at www.globalpaymentsinc.com free of charge. Certain materials relating to our corporate governance, including our codes of ethics applicable to our directors, senior financial officers and other employees, are also available in the investor relations section of our website. Copies of our filings, specified exhibits and corporate governance materials are also available, free of charge, by writing us using the address on the cover of this Annual Report on Form 10-K. You may also telephone our investor relations office directly at (770) 829-8478. We are not including the information on our website as a part of, or incorporating it by reference into, this Annual Report on Form 10-K.

Our SEC filings may also be viewed and copied at the following SEC public reference room and at the offices of the New York Stock Exchange.

SEC Public Reference Room

100 F Street, N.E.

Washington, DC 20549

(You may call the SEC at 1-800-SEC-0330 for further information on the public reference room.)

NYSE Euronext

20 Broad Street

New York, NY 10005

ITEM 1A - RISK FACTORS

An investment in our common stock involves a high degree of risk. You should consider carefully the following risks and other information contained in this Annual Report on Form 10-K and other SEC filings before you decide whether to buy our common stock. The risks identified below are not all encompassing but should be considered in establishing an opinion of our future operations. If any of the events contemplated by the following discussion of risks should occur, our business, results of operations, financial condition and cash flows could suffer significantly. As a result, the market price of our common stock could decline and you may lose all or part of your investment in our common stock.

Risks Related to Our Business and Operations

Our ability to protect our systems and data from continually evolving cybersecurity risks or other technological risks could affect our reputation among our customers and cardholders, adversely affect our continued card network registration or membership and financial institution sponsorship, and may expose us to penalties, fines, liabilities and legal claims.

In order to provide our services, we process and store sensitive business information and personal information about our merchants, merchants’ customers, merchants’ employees, ISOs, vendors, partners and other parties. This information may include credit and debit card numbers, bank account numbers, social security numbers, driver’s license numbers, names and addresses, and other types of personal information or sensitive business information. Some of this information is also processed and stored by our third-party service providers to whom we outsource certain functions and other agents (which we refer to collectively as our "associated third parties") as well as merchants and ISOs. We have responsibility to the card networks, their member financial institutions, and in some instances, our merchants, ISOs and/or individuals, for our failure or the failure of our associated third parties to protect this information.

We are a regular target of malicious third-party attempts to identify and exploit system vulnerabilities, and/or penetrate or bypass our security measures, in order to gain unauthorized access to our networks and systems or those of our associated third parties. Such access could lead to the compromise of sensitive, business, personal or confidential information. As a result, we follow a defense-in-depth model for cybersecurity, meaning we proactively seek to employ multiple methods at different layers to defend our systems against intrusion and attack and to protect the data we collect. However, we cannot be certain that these measures will be successful and will be sufficient to counter all current and emerging technology threats.

Our computer systems and/or our associated third parties’ computer systems could be subject to penetration, and our data protection measures may not prevent unauthorized access. The techniques used to obtain unauthorized access, disable or degrade service or sabotage systems change frequently and are often difficult to detect. Threats to our systems and our associated third parties’ systems can derive from human error, fraud or malice on the part of employees or third parties, or may result from accidental technological failure. Computer viruses and other malware can be distributed and could infiltrate our systems or those of our associated third parties. In addition, denial of service or other attacks could be launched against us for a variety of purposes, including to interfere with our services or create a diversion for other malicious activities. Our defensive measures may not prevent downtime, unauthorized access or use of sensitive data. While we maintain first- and third-party insurance coverage that may cover certain aspects of cyber risks, such insurance coverage may be insufficient to cover all losses. Further, while we select our associated third parties carefully, we do not control their actions. Any problems experienced by these third parties, including those resulting from breakdowns or other disruptions in the services provided by such parties or cyberattacks and security breaches, could adversely affect our ability to service our merchant customers or otherwise conduct our business.

We also could be subject to liability for claims relating to misuse of personal information in violation of contractual obligations or data privacy laws. Regulatory authorities around the world are considering or have enacted a number of legislative and regulatory proposals concerning data protection and use, and the interpretation and application of consumer and data protection laws in the United States, Europe, the Asia-Pacific region and elsewhere is increasingly uncertain. It is possible that these laws may be interpreted and applied in a manner that is inconsistent with our data practices or operations model, which could result in potential liability for fines, damages or a need to incur substantial costs to modify our operations. In addition, we cannot provide assurance that the contractual requirements related to use, security and privacy that we impose on our associated third parties who have access to this data will be followed or will be adequate to prevent the misuse of this data. Any misuse or compromise of personal information or failure to adequately enforce these contractual requirements could result in liability, protracted and costly litigation and, with respect to misuse of personal information of our merchants and consumers, lost revenue and reputational harm.

Any type of security breach, attack or misuse of data described above or otherwise, whether experienced by us or an associated third party, could harm our reputation and deter existing and prospective customers from using our services or from making electronic payments generally, increase our operating expenses in order to contain and remediate the incident, expose us to unanticipated or uninsured liability, disrupt our operations (including potential service interruptions), distract our management,

increase our risk of litigation or regulatory scrutiny, result in the imposition of penalties and fines under state, federal and foreign laws or by the card networks, and adversely affect our continued card network registration or membership and financial institution sponsorship. Our removal from networks' lists of Payment Card Industry Data Security Standard compliant service providers could mean that existing merchant customers, sales partners or other third parties may cease using or referring our services. Also, prospective merchant customers, sales partners or other third parties may choose to terminate negotiations with us, or delay or choose not to consider us for their processing needs. In addition, the card networks could refuse to allow us to process through their networks.

The payment processing industry is highly competitive, and some of our competitors are larger and have greater financial and operational resources than we do, which may give them an advantage with respect to the pricing of services offered to customers and the ability to develop new technologies.

We operate in the electronic payments market, which is highly competitive. In this market, our primary competitors include other independent payment processors, as well as financial institutions, ISOs and, potentially, card networks. Many of our competitors are companies that are larger than we are, with greater financial and operational resources than we have. Our competitors that are financial institutions or subsidiaries of financial institutions do not incur the costs associated with being sponsored by a direct member for participation in the card networks, as we do in certain jurisdictions, and may be able to settle transactions more quickly for merchants than we can. These financial institutions may also provide payment processing services to merchants at a loss in order to generate banking fees from the merchants. It is also possible that larger financial institutions could decide to perform in-house some or all of the services that we currently provide or could provide. These attributes may provide them with a competitive advantage in the market.

Furthermore, we are facing increasing competition from nontraditional competitors, including new entrant technology companies who offer certain innovations in payment methods. Some of these competitors utilize proprietary software and service solutions. Some of these nontraditional competitors have significant financial resources and robust networks and are highly regarded by consumers. In addition, some nontraditional competitors, such as private companies or startup companies, may be less risk averse than we are and, therefore, may be able to respond more quickly to market demands. If these nontraditional competitors gain a greater share of total electronic payments transactions, it could have a material adverse effect on our business, financial condition, results of operations and cash flows. These competitors may compete in ways that minimize or remove the role of traditional card networks, processors and/or point-of-sale software in the electronic payments process.

In order to remain competitive and to continue to increase our revenues and earnings, we must continually and quickly update our services, a process that could result in higher costs and the loss of revenues, earnings and customers if the new services do not perform as intended or are not accepted in the marketplace.

The electronic payments markets in which we compete are characterized by rapid technological change, new product introductions, evolving industry standards and changing customer needs. In order to remain competitive, we are continually involved in a number of projects, including the development of a new authorization platform, mobile payment applications, ecommerce services and other new offerings emerging in the electronic payments industry. These projects carry the risks associated with any development effort, including cost overruns, delays in delivery and performance problems. In the electronic payments markets, these risks are even more acute. Any delay in the delivery of new services or the failure to differentiate our services could render our services less desirable to customers, or possibly even obsolete. Furthermore, as the market for alternative payment processing services evolves, it may develop too rapidly or not rapidly enough for us to recover the costs we have incurred in developing new services targeted at this market.

In addition, the services we deliver to the electronic payments markets are designed to process very complex transactions and deliver reports and other information on those transactions, all at very high volumes and processing speeds. Any failure to deliver an effective and secure product or any performance issue that arises with a new product or service could result in significant processing or reporting errors or other losses. As a result of these factors, our development efforts could result in higher costs that could reduce our earnings in addition to a loss of revenues and earnings if promised new services are not delivered timely to our customers or do not perform as anticipated. We rely in part on third parties, including some of our competitors and potential competitors, for the development of and access to new technologies.

Our revenues from the sale of services to merchants that accept Visa cards and MasterCard cards are dependent upon our continued Visa and MasterCard registrations, financial institution sponsorship and, in some cases, continued membership in certain card networks.

In order to provide our Visa and MasterCard transaction processing services, we must be either a direct member or be registered as a merchant processor or service provider of Visa and MasterCard, respectively. Registration as a merchant processor

or service provider is dependent upon our being sponsored by Members of each organization in certain jurisdictions. If our sponsor financial institution in any market should stop providing sponsorship for us, we would need to find another financial institution to provide those services or we would need to attain direct membership with the card networks, either of which could prove to be difficult and expensive. If we are unable to find a replacement financial institution to provide sponsorship or attain direct membership, we may no longer be able to provide processing services to affected customers and potential customers in that market, which would negatively affect our revenues, earnings and cash flows. Furthermore, some agreements with our financial institution sponsors give them substantial discretion in approving certain aspects of our business practices, including our solicitation, application and qualification procedures for merchants and the terms of our agreements with merchants. Our sponsors' discretionary actions under these agreements could have a material adverse effect on our business, financial condition, results of operations and cash flows. In connection with direct membership, the rules and regulations of various card associations and networks prescribe certain capital requirements. Any increase in the capital level required would limit our use of capital for other purposes.

We rely on various financial institutions to provide clearing services in connection with our settlement activities. If we are unable to maintain clearing services with these financial institutions and are unable to find a replacement, our business may be adversely affected.

We rely on various financial institutions to provide clearing services in connection with our settlement activities. If such financial institutions should stop providing clearing services, we must find other financial institutions to provide those services. If we are unable to find a replacement financial institution we may no longer be able to provide processing services to certain customers, which could negatively affect our revenues, earnings and cash flows.

If we fail to comply with the applicable requirements of the card networks, they could seek to fine us, suspend us or terminate our registrations or membership. If we incur fines or penalties for which our merchants or ISOs are responsible that we cannot collect or pursue collection from them, we may have to bear the cost of such fines or penalties.

We are subject to card association and network rules that could subject us to a variety of fines or penalties that may be levied by the card networks for certain acts or omissions. The rules of the card networks are set by their boards, which may be influenced by card issuers, and some of those issuers are our competitors with respect to these processing services. Many banks directly or indirectly sell processing services to merchants in direct competition with us. These banks could attempt, by virtue of their influence on the networks, to alter the networks' rules or policies to the detriment of non-members, including us in certain jurisdictions. The termination of our registrations or our membership or our status as a service provider or a merchant processor, or any changes in card association or other network rules or standards, including interpretation and implementation of the rules or standards, that increase the cost of doing business or limit our ability to provide transaction processing services to our customers, could have a material adverse effect on our business, operating results, financial condition and cash flows. If a merchant or an ISO fails to comply with the applicable requirements of the card associations and networks, we or the merchant or ISO could be subject to a variety of fines or penalties that may be levied by the card associations or networks. If we cannot collect or pursue collection of such amounts from the applicable merchant or ISO, we may have to bear the cost of such fines or penalties, resulting in lower earnings for us. The termination of our registration, or any changes in the Visa or MasterCard rules that would impair our registration, could require us to stop providing Visa and MasterCard payment processing services, which would make it impossible for us to conduct our business on its current scale.

Our systems or our third-party providers' systems may fail, which could interrupt our service, cause us to lose business, increase our costs and expose us to liability.

We depend on the efficient and uninterrupted operation of our computer systems, software, data centers and telecommunications networks, as well as the systems and services of third parties. A system outage or data loss could have a material adverse effect on our business, financial condition, results of operations and cash flows. Not only would we suffer damage to our reputation in the event of a system outage or data loss, but we may also be liable to third parties. Our systems and operations or those of our third-party providers could be exposed to damage or interruption from, among other things, fire, natural disaster, power loss, telecommunications failure, terrorist acts, war, unauthorized entry, human error, and computer viruses or other defects. Defects in our systems or those of third parties, errors or delays in the processing of payment transactions, telecommunications failures, or other difficulties (including those related to system relocation) could result in loss of revenue, loss of customers, loss of merchant and cardholder data, harm to our business or reputation, exposure to fraud losses or other liabilities, negative publicity, additional operating and development costs, fines and other sanctions imposed by card networks, and/or diversion of technical and other resources.

We may experience software defects, undetected errors, and development delays, which could damage customer relations, decrease our potential profitability and expose us to liability.

Our services are based on sophisticated software and computing systems that often encounter development delays, and the underlying software may contain undetected errors, viruses or defects. Defects in our software services and errors or delays in our processing of electronic transactions could result in additional development costs, diversion of technical and other resources from our other development efforts, loss of credibility with current or potential customers, harm to our reputation and exposure to liability claims.

In addition, we rely on technologies and software supplied by third parties that may also contain undetected errors, viruses or defects that could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Increased merchant, referral partner or ISO attrition could cause our financial results to decline.

We experience attrition in merchant credit and debit card processing volume resulting from several factors, including business closures, transfers of merchants' accounts to our competitors, unsuccessful contract renewal negotiations and account closures that we initiate for various reasons, such as heightened credit risks or contract breaches by merchants. If an ISO partner switches to another transaction processor, terminates our services, internalizes payment processing functions that we perform, merges with or is acquired by one of our competitors, or shuts down or becomes insolvent, we may no longer receive new merchant referrals from the ISO, and we risk losing existing merchants that were originally enrolled by the ISO. We cannot predict the level of attrition in the future and it could increase. Our referral partners are a significant source of new business. Higher than expected attrition could negatively affect our results, which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Our future growth depends in part on the continued expansion of markets in which we already operate, the emergence of new markets, and the continued availability of alliance relationships and strategic acquisition opportunities.

Our future growth and profitability depend upon our continued expansion within the markets in which we currently operate, the further expansion of these markets, the emergence of other markets for electronic transaction payment processing and our ability to penetrate these markets. As part of our strategy to achieve this expansion, we look for acquisition opportunities, investments and alliance relationships with other businesses that will allow us to increase our market penetration, technological capabilities, product offerings and distribution capabilities. We may not be able to successfully identify suitable acquisition, investment and alliance candidates in the future, and if we do, they may not provide us with the value and benefits we anticipate.

Our expansion into new markets is also dependent upon our ability to apply our existing technology or to develop new applications to meet the particular service needs of each new market. We may not have adequate financial or technological resources to develop effective and secure services and distribution channels that will satisfy the demands of these new markets. If we fail to expand into new and existing electronic payments markets, we may not be able to continue to grow our revenues and earnings.

There may be a decline in the use of cards and other electronic payments as a payment mechanism for consumers or adverse developments with respect to the card industry in general.

If consumers do not continue to use credit or debit cards or other electronic payment methods as a payment mechanism for their transactions or if there is a change in the mix of payments between cash, checks, credit cards, and debit cards, which is adverse to us, it could have a material adverse effect on our business, financial condition, results of operations and cash flows. Consumer credit risk may make it more difficult or expensive for consumers to gain access to credit facilities such as credit cards. Regulatory changes may result in financial institutions seeking to charge their customers additional fees for use of credit or debit cards. Such fees may result in decreased use of credit or debit cards by cardholders. In each case, our business, financial condition, results of operations and cash flows may be adversely affected. We believe future growth in the use of credit and debit cards and other electronic payments will be driven by the cost, ease-of-use, and quality of services offered to consumers and businesses. In order to consistently increase and maintain our profitability, consumers and businesses must continue to use electronic payment methods that we process, including credit and debit cards.

We incur chargeback losses when our merchants refuse or cannot reimburse us for chargebacks resolved in favor of their customers. Any increase in chargebacks not paid by our merchants may adversely affect our results of operations, financial condition and cash flows.

In the event a dispute between a cardholder and a merchant is not resolved in favor of the merchant, the transaction is normally charged back to the merchant and the purchase price is credited or otherwise refunded to the cardholder. If we are unable to collect

such amounts from the merchant's account or reserve account (if applicable), or if the merchant refuses or is unable, due to closure, bankruptcy or other reasons, to reimburse us for a chargeback, we bear the loss for the amount of the refund paid to the cardholder. The risk of chargebacks is typically greater with those merchants that promise future delivery of goods and services rather than delivering goods or rendering services at the time of payment. We may experience significant losses from chargebacks in the future. Any increase in chargebacks not paid by our merchants could have a material adverse effect on our business, financial condition, results of operations and cash flows. We have policies to manage merchant-related credit risk and often mitigate such risk by requiring collateral and monitoring transaction activity. Notwithstanding our programs and policies for managing credit risk, it is possible that a default on such obligations by one or more of our merchants could have a material adverse effect on our business.

Fraud by merchants or others could have an adverse effect on our operating results, financial condition and cash flows.

We have potential liability for fraudulent electronic payment transactions or credits initiated by merchants or others. Examples of merchant fraud include when a merchant or other party knowingly uses a stolen or counterfeit credit or debit card, card number, or other credentials to record a false sales or credit transaction, processes an invalid card, or intentionally fails to deliver the merchandise or services sold in an otherwise valid transaction. Criminals are using increasingly sophisticated methods to engage in illegal activities such as counterfeiting and fraud. Failure to effectively manage risk and prevent fraud could increase our chargeback losses or cause us to incur other liabilities. It is possible that incidents of fraud could increase in the future. Increases in chargebacks or other liabilities could have a material adverse effect on our operating results, financial condition and cash flows.

We are subject to economic and political risk, the business cycles and credit risk of our customers and the overall level of consumer, business and government spending, which could negatively affect our business, financial condition, results of operations and cash flows.

The global electronic payments industry depends heavily on the overall level of consumer, business and government spending. We are exposed to general economic conditions that affect consumer confidence, consumer spending, consumer discretionary income and changes in consumer purchasing habits. A sustained deterioration in general economic conditions in the markets in which we operate or increases in interest rates may adversely affect our financial performance by reducing the number or average purchase amount of transactions made using electronic payments. A reduction in the amount of consumer spending could result in a decrease in our revenues and profits. If our merchants make fewer sales to consumers using electronic payments or consumers using electronic payments spend less per transaction, we will have fewer transactions to process or lower transaction amounts, each of which would contribute to lower revenues.

A downturn in the economy could force retailers to close, resulting in exposure to potential credit losses and future transaction declines. Furthermore, credit card issuers may reduce credit limits and be more selective with respect to whom they issue credit cards. We also have a certain amount of fixed and other costs, including rent, debt service, and salaries, which could limit our ability to quickly adjust costs and respond to changes in our business and the economy. Changes in economic conditions could also adversely affect our future revenues and profits and cause a materially adverse effect on our business, financial condition, results of operations and cash flows.

In addition, a recessionary economic environment could affect our merchants through a higher rate of bankruptcy filings, resulting in lower revenues and earnings for us. Our associated third parties are also liable for any fines or penalties that may be assessed by any card networks. In the event that we are not able to collect such amounts from our merchants or the associated third parties, due to fraud, breach of contract, insolvency, bankruptcy or any other reason, we may be liable for any such charges.

Reject losses arise from the fact that, in most markets, we collect our fees from our merchants on the first day after the monthly billing period. This results in the build-up of a substantial receivable from our customers. If a merchant has gone out of business during the billing period, we may be unable to collect such fees, which could negatively affect our business, financial condition, results of operations and cash flows.

Increases in card network fees may result in the loss of customers and/or a reduction in our earnings.

From time-to-time, the card networks, including Visa and MasterCard, increase the fees that they charge processors. We could attempt to pass these increases along to our merchant customers, but this strategy might result in the loss of customers to our competitors who may not pass along the increases, thereby reducing our revenues and earnings. If competitive practices prevent us from passing along the higher fees to our merchant customers in the future, we may have to absorb all or a portion of such increases, thereby increase our operating costs and reducing our earnings.

Any new implementation of or changes made to laws, regulations, card network rules or other industry standards affecting our business in any of the geographic regions in which we operate may require significant development efforts or have an unfavorable effect on our financial results and our cash flows.